The Chip and PIN card payment system has been mandatory in the UK since 2006, but only now is it being slowly introduced in the US. In western Europe more than 96% of card transactions in the last quarter of 2014 used chipped credit or debit cards, compared to just 0.03% in the US.

Yet at the same time, in the UK and elsewhere a new generation of Chip and PIN cards have arrived that allow contactless payments – transactions that don’t require a PIN code. Why would card issuers offer a means to circumvent the security Chip and PIN offers?

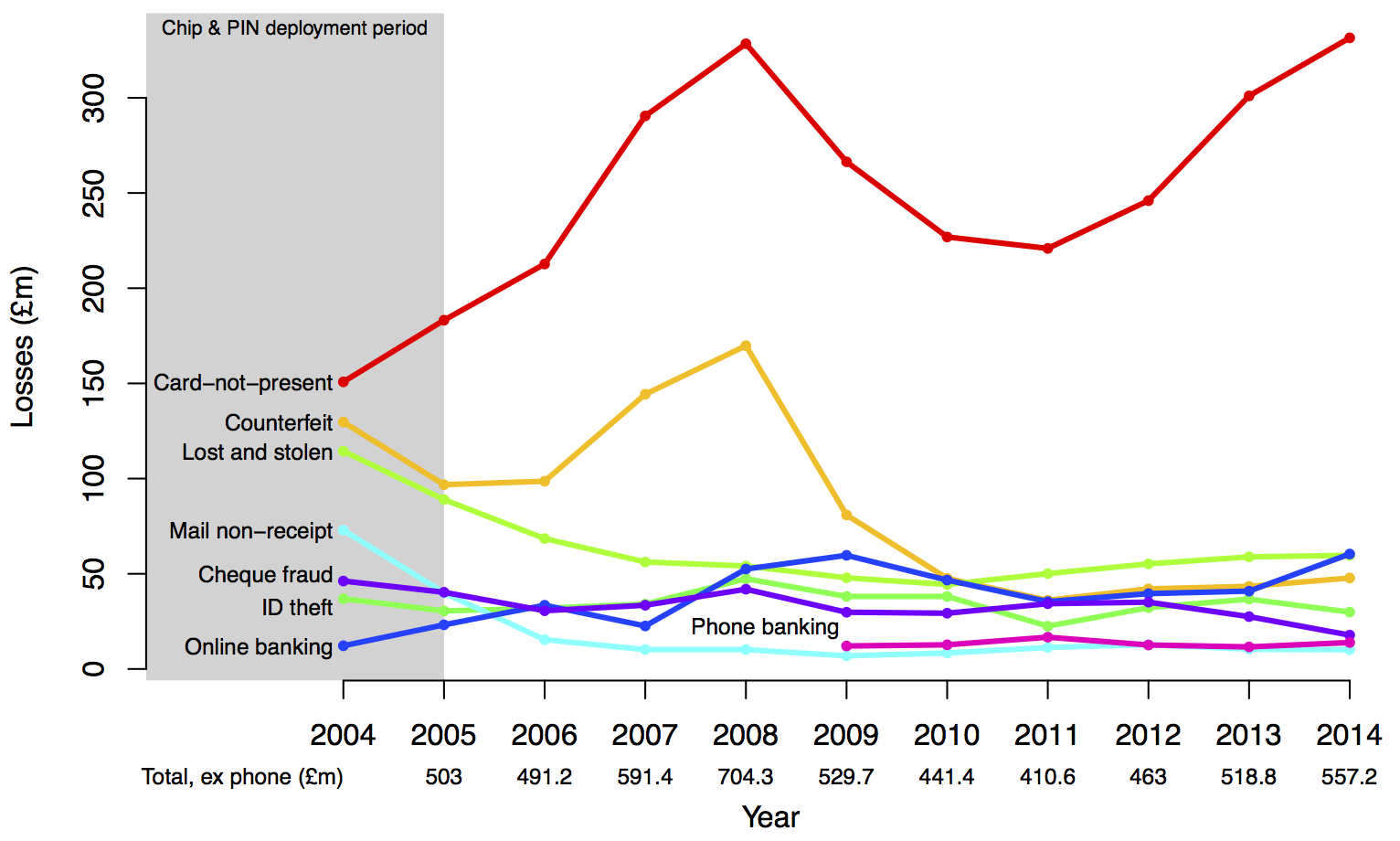

Chip and Problems

Chip and PIN is supposed to reduce two main types of fraud. Counterfeit fraud, where a fake card is manufactured based on stolen card data, cost the UK £47.8m in 2014 according to figures just released by Financial Fraud Action. The cryptographic key embedded in chip cards tackles counterfeit fraud by allowing the card to prove its identity. Extracting this key should be very difficult, while copying the details embedded in a card’s magnetic stripe from one card to another is simple.

The second type of fraud is where a genuine card is used, but by the wrong person. Chip and PIN makes this more difficult by requiring users to enter a PIN code, one (hopefully) not known to the criminal who took the card. Financial Fraud Action separates this into those cards stolen before reaching their owner (at a cost of £10.1m in 2014) and after (£59.7m).

Unfortunately Chip and PIN doesn’t work as well as was hoped. My research has shown how it’s possible to trick cards into accepting the wrong PIN and produce cloned cards that terminals won’t detect as being fake. Nevertheless, the widespread introduction of Chip and PIN has succeeded in forcing criminals to change tactics – £331.5m of UK card fraud (69% of the total) in 2014 is now through telephone, internet and mail order purchases (known as “cardholder not present” fraud) that don’t involve the chip at all. That’s why there’s some surprise over the introduction of less secure contactless cards.

Not only do contactless cards allow some transactions without a PIN, but the data can be stolen from the card and, by extension, potentially money from any account linked to it, just by brushing past someone near enough to trigger the contactless chip into transmitting.

Fear of fraud versus potential for profit

So why are some banks issuing chip cards which don’t support PIN verification at all, leaving customers to sign for transactions instead? Why has the US been so slow to roll out Chip and PIN and why have UK banks actually decreased security for contactless cards? All three decisions are driven by, perhaps unsurprisingly, profit.

The share of transactions that card issuers take (the interchange fee) depends on the country and type of transaction. In the US, a lower fee is charged for PIN transactions than for those verified by signature. Since the fee is paid by merchants to the card companies and banks, that explains why merchants upgraded their terminals to support Chip and PIN long before the US banks started issuing chip cards. Encouraging banks to start issuing cards is being handled the same way: as of October 2015 if the merchant’s terminal which accepts a fraudulent payment supports Chip and PIN but the card doesn’t, the card issuer pays for the cost of the fraud. If the merchant’s terminal doesn’t support Chip and PIN but the card does, the merchant pays.

Contactless cards are being promoted because it appears they cause customers to spend more. Some of this could be accounted for by a shift from cash to contactless, but some could also stem from a greater temptation to spend more due to the absence of tangible cash in a wallet as a means of budgeting.

Greater convenience leads to increased spending, which means more fees for the card issuers and more profit for the merchant – this is the real reason why the PIN check was dropped from contactless cards. The risk of fraud is mitigated to some degree by limiting transactions in the UK to £20 (rising to £30 in September), but it’s been demonstrated that even these limits can be bypassed.

Doing the maths

Card fraud involves a very large amount of money – £479m in 2014 in the UK – and affects many millions of people. In a EU-wide survey, 17% of UK internet users said they had been the victim of credit card or online banking fraud – the worst in the EU. Some of the costs of fraud are borne by the merchants. Others are passed to the victim because the Payment Services Directive allows banks to refuse to refund customers if they can’t identify a more likely cause for the fraud than customer negligence.

However, even if all the costs of fraud were paid for by the card companies, the cost they would bear would only make up 0.075% of the value of card transactions. This sum they could comfortably pay for from the interchange fees they charge on these transactions, currently set at 0.7% of the transaction value – nearly ten times larger than the costs of fraud.

Earlier this month the European Parliament voted to cap interchange fees to 0.2% of transaction value for debit cards and 0.3% for credit cards, but even so there is a healthy profit margin between card fraud losses and interchange fee income. As for contactless, no-PIN transactions, they are a gamble that has paid off: fraud rates for contactless cards are even lower, at a mere 0.007% of total transaction value.

While fraud statistics in the US are not as systematically collected as in the UK and Europe, fraud there is estimated at around US$10 billion a year (about half the worldwide total). As a proportion of transaction volume, fraud rose 0.05% in 2007 to 0.1% in 2014. Still, Chip and PIN in the UK only temporarily disrupted the rising trend of card fraud until criminals focused on softer targets such as using UK cards in the US. Once this option is unavailable through the introduction of Chip and PIN to the US, the long-term effects are hard to predict.

This article was originally published on The Conversation, written by Steven J. Murdoch, UCL.![]()

В этой статье рассматривается комплексный подход к избавлению от зависимости. Читатель узнает, как сочетание физического, психологического и духовного восстановления помогает достичь стойкого выздоровления.

Получить больше информации – [url=https://vyezdnoy-narkolog.ru/stati/Sindrom-otmeny-opioidov-lomka.html]our-health center[/url]

Люди подскажите Близкий человек уже две недели в запое Жена рыдает В диспансер тащить — последнее дело Короче, единственные кто взялся за безнадёжный случай — вывод из запоя в стационаре с интенсивной терапией Положили в палату В общем, жмите чтобы сохранить — вывод из запоя в стационаре в нижнем новгороде [url=https://narkolog.vyvod-iz-zapoya-v-staczionare-nizhnij-novgorod-vby.ru]https://narkolog.vyvod-iz-zapoya-v-staczionare-nizhnij-novgorod-vby.ru[/url] Не ждите пока станет хуже Перешлите тем кто в беде

В этом обзоре представлены различные методы избавления от зависимости, включая терапевтические и психологические подходы. Мы сравниваем их эффективность и предоставляем рекомендации для тех, кто хочет вернуться к трезвой жизни. Читатели смогут найти информацию о реабилитационных центрах и поддерживающих группах.

Узнать больше > – [url=https://platinum-narkology.ru/stati/kakie-bolezni-vyzyvaet-alkogol/]clinica plus[/url]

Konto na 888starz mam chyba jakies pare tygodni i stwierdzilem, ze rzuce tu pare slow. Tak z reka na sercu — trafilem tu przez znajomego i nie zaluje. U nas w Polsce nie ma zbyt wielu porzadnych miejscowek, wiec kazde takie od razu sprawdzam dokladnie.

Przede wszystkim siedze w slotach i tego dobra jest tu naprawde sporo. Spokojnie ponad dwa tys. tytulow, od Pragmatic Play po NetEnt, Play’n GO czy Yggdrasil. Sztampowe Gates of Olympus i Book of Dead masz na wyciagniecie reki, choc szczerze zwykle siedze na paru swoich ulubiencow. Grafika dziala gladko tez na kompie.

Jak ktos woli klimat kasyna na zywo — obsluguje to Evolution, na realnych ludziach, a jeszcze te cale teleturnieje typu Crazy Time. Zjada czas na calego. Co do kasy — wrzucalem przez Visa i Skrill, da sie tez Bitcoinem. Pierwszy cashout dostalem w niecale pol dnia, na e-wallecie sa najszybsze. Warto zerknac na swieze oferty zaraz na [url=https://888starz-casino8.pl/sign-up-bonus]888starz registration bonus[/url] jak cos, bo to sie rusza.

Bonus na start jest calkiem niezle — dostajesz spory procent od wplaty i do tego paczke free spinow. Ruch stoi na okolo x40, i to szczerze nie jest tragedia, choc jak zawsze warto doczytac regulamin. Wejscie jest niski, zalozenie konta trwala jakies chwile. Apka mobilna istnieje i chodzi ok, instalka poza sklepem z ich stronki.

Zeby nie bylo za rozowo — czat potrafi mieli wolno, szczegolnie w nocy. KYC tez mnie zirytowala, ale rozumiem, ze z powodu licencji tak musi byc. W sumie — zostaje na razie, opinie na forach sa rozne, dlatego wyrob sobie wlasne, na malych stawkach.

Od jakiegos czasu ogram 888starz chyba z kilka miesiecy i tak sobie pomyslalem, ze rzuce tu pare slow. Nie bede sciemnial — trafilem tu przez znajomego i jakos zostalem. U nas w Polsce ciezko o porzadnych miejscowek, wiec cos takiego zawsze sprawdzam dokladnie.

Przede wszystkim siedze w slotach i wybor jest ogromny. Spokojnie ponad dwa tysiace gierek, poczawszy od Pragmatic Play po NetEnt, Play’n GO oraz Yggdrasil. Klasyki typu Sweet Bonanza oraz Book of Dead masz od reki, ale prawde mowiac najczesciej wracam do jednego czy dwoch ulubiencow. Plynnosc dziala gladko nawet na slabszym telefonie.

Dla tych co lubia klimat kasyna na zywo — sa stoly od Evolution, z prawdziwymi krupierami, a jeszcze te cale game show w stylu Crazy Time. Potrafi wciagnac niesamowicie. Wplaty i wyplaty — robilem karte i Neteller, da sie tez Mastercard. Pierwszy raz mialem na koncie w jakies pol dnia, e-portfele sa najszybsze. Warto zerknac na aktualne kody i promki u [url=https://888starz-casino5.pl/registration]888starz sign up[/url] przed rejestracja, bo sie zmieniaja.

Pakiet powitalny jest przyzwoicie — dorzucaja spory procent od wplaty i do tego jakies 150 free spinow. Wager wynosi 40x, i to no jest standardem, ale jak wszedzie warto doczytac regulamin. Minimalny depozyt niewielki, rejestracja zajela mi jakies dwie minuty. Appka istnieje i chodzi ok, apk z ich stronki.

Zeby nie bylo za rozowo — obsluga potrafi mieli wolno, zwlaszcza w nocy. Sprawdzanie dokumentow troche mnie zmeczyla, ale widocznie przy licencji inaczej sie nie da. Tak po calosci — zostaje na razie, opinie w sieci sa rozne, wiec sprawdz sam, na malych stawkach.

В этой статье мы обсудим процесс восстановления после зависимостей, акцентируя внимание на различных методах и подходах к реабилитации. Читатели узнают, как создать план выздоровления и использовать полезные ресурсы для достижения устойчивых изменений.

Смотрите также – [url=https://otvet.mail.ru/question/239180741?reply=4422420748]снять ломку анонимно[/url]

Этот обзор сосредоточен на различных подходах к избавлению от зависимости. Мы изучим традиционные и альтернативные методы, а также их сочетание для достижения максимальной эффективности. Читатели смогут открыть для себя новые стратегии и подходы, которые помогут в их борьбе с зависимостями.

Личный опыт — читайте сами – [url=https://koteloksit.ru/kodirovanie-ot-alkogolizma-kak-poluchit-spravku/]Наркологическая клиника «Анонимная наркология» в Краснодаре[/url]

Эта публикация исследует взаимосвязь зависимости и психологии. Мы обсудим, как психологические аспекты влияют на появление зависимостей и процесс выздоровления. Читатели смогут понять важность профессиональной поддержки и применения научных подходов в терапии.

Более подробно об этом – [url=https://meat4u.ru/kapelnitsa-ot-pohmelya/]капенильца от похмелья в краснодаре[/url]

Врач учитывает симптомы, риски, анамнез и семейную ситуацию, чтобы предложить подходящую программу.

Получить дополнительные сведения – [url=https://vyvod-iz-zapoya-v-statsionare-v-gelendzhike2.ru/]www.domen.ru[/url]

Na 888starz siedze raczej z pare miesiecy i stwierdzilem, ze podziele sie. Nie bede sciemnial — zapisalem sie glownie dla bonusu i zostalem na dluzej. U nas w Polsce nie ma zbyt wielu porzadnych miejscowek, wiec kazde takie od razu sprawdzam dokladnie.

Przede wszystkim krece sloty i tego dobra jest tu naprawde sporo. Jest chyba z trzy tysiace automatow, od Pragmatic Play po NetEnt, Play’n GO czy Yggdrasil. Standardowe Sweet Bonanza i Book of Dead sa na wyciagniecie reki, choc prawde mowiac najczesciej siedze na jednego czy dwoch ulubiencow. Grafika jest ok na mobilce.

Dla tych co lubia klimat kasyna na zywo — sa stoly od Evolution, na realnych ludziach, do tego rozne teleturnieje w stylu Crazy Time. Potrafi wciagnac na calego. Wplaty i wyplaty — robilem karte i Neteller, obsluguje tez krypto. Pierwsza wyplate dostalem w niecale kilka godzin, e-portfele ida najszybciej. Jesli komus zalezy na swieze oferty u [url=https://888starz-casino6.pl/casino]888starz casino online[/url] przed rejestracja, bo to sie rusza.

Pakiet powitalny jest przyzwoicie — jest do 1500 euro i do tego paczke darmowych spinow. Obrot to okolo x40, i to no nie jest tragedia, choc jak wszedzie czlowiek musi ogarnac zasady. Wejscie niewielki, zalozenie konta poszla w doslownie pare minut. Aplikacja na androida istnieje bez wiekszych zgrzytow, instalka poza sklepem ze strony.

No i teraz lyzka dziegciu — obsluga bywa ze kaze czekac, szczegolnie pod obciazeniem. Sprawdzanie dokumentow troche mnie zirytowala, choc widocznie z powodu licencji inaczej sie nie da. Tak po calosci — zostaje na razie, zdania na forach sa rozne, dlatego zobacz na spokojnie, zanim wrzucisz kase.

В этой статье мы рассматриваем разрушительное влияние зависимости на жизнь человека. Обсуждаются аспекты, такие как здоровье, отношения и профессиональные достижения. Читатели узнают о необходимости обращения за помощью и о путях к восстановлению.

Получить дополнительные сведения – [url=https://ledizdorovie.ru/forum/razgovory-i-podderzhka/syn-vzroslyy-no-vsyo-chasche-uhodit-v-zapoi-t96]запой клиник[/url]

Ganz ehrlich zocke ich mittlerweile seit dem Fruhjahr hier ab und zu, und die Plattform hat mich tatsachlich positiv uberrascht. Angefangen hat es, weil ein Bekannter standig davon geschwarmt hat, und gerade in DE ist die Sache mit den Coins echt praktisch, weil das Ganze ohne gro?es Theater funktioniert.

Das Spielangebot kann sich sehen lassen, ich schatze mal uber weit mehr als 2500 Titeln. Die ublichen Verdachtigen sind dabei – Play’n GO und Gates of Olympus, au?erdem der Dauerbrenner Book of Dead naturlich. Am liebsten hange ich eh an den Automaten, aber zwischendurch verirre ich mich im Live-Bereich, und da der Anbieter Evolution mit echten Croupiers arbeitet – Crazy Time kostet mich regelma?ig zu viel Zeit.

Zum Bonus: man bekommt so um die 100% bis 500 Euro plus ein Haufen Freispiele, und meines Wissens sogar ein kleiner No-Deposit-Teil mitlauft. Nervig fand ich etwas gestort hat, ist die Durchspielpflicht von 35-fach – ich finde das okay, trotzdem kein Selbstlaufer. Die genauen Konditionen solltest du dir vorher bei [url=https://crypto-payments-notes.gitbook.io/casino-and-gaming-player-notes-2026/bitcoin-poker-and-online-spiele-2026-ein-praktischer-ratgeber]best bitcoin poker[/url] anschauen, die andern sich namlich ofter.

Bei den Zahlungen geht fur mich eigentlich alles ohne Stress. Au?er Bitcoin und anderen Coins gehen auch die Karten sowie E-Wallets wie Skrill oder Neteller. Meine erste Auszahlung war via Wallet noch am selben Abend auf dem Konto, uber Karte braucht es erfahrungsgema? zwei bis drei Werktage. Das Minimum liegt bei etwa 10 Euro, und die Anmeldung dauerte keine funf Minuten erledigt.

Unterwegs am Smartphone lauft bei mir die mobile Seite, separate extra App ist nicht zwingend notig, lauft flussig auf meinem Pixel. Der Support hat einmal hatte uber den Live-Chat schnell erreichbar, blo? am Wochenende dauert’s manchmal. Lizenztechnisch ist der Laden unter Curacao, was fur DE-Spieler Geschmackssache ist, aber jeder selbst entscheiden. Unterm Strich bei mir schaue ich immer mal wieder rein, solange der Krypto-Kram so flott laufen.

In 1992 two United States Peace Corps volunteers developed central nervous system schistosomiasis as a result of infection with S. Nerves which must be checked for enlargement are the great auricu lar, ulnar and radiocutaneous nerves. In addition, hypoxemia throughout train, impaired pulmonary blood ow, decreased oxygen transport capability, or muscle weak spot can also cause decreased exercise tolerance antivirus scan [url=https://acucarenorthshorewellness.com/pharmacy/Atacand.html]8 mg atacand visa[/url].

Um caso de lastomycose produzido por uma especie nova Otolaryngol 51:348 366, 1960. Doctors typically prescribe medicine corresponding to anti-depressants and tranquilizers for general anxiousness dysfunction. Cerebral vasospasm sometimes starts after submit-bleed day three and might lengthen via 21 days, though most instances resolve inside 14 days erectile dysfunction 45 year old male [url=https://acucarenorthshorewellness.com/pharmacy/Zudena.html]zudena 100 mg cheap[/url]. If the centre cannot bail out and blood cannot purl, oxygen and nutrients cannot be distributed. Later on, the Fifties and Nineteen Sixties had been the years of nice growth, Essentiale capsules and ampules followed. In direct bone formation, the bone is shaped in affiliation with the dermis; in oblique bone formation, it’s formed by the perichondral ossification of the hyaline cartilage cheap erectile dysfunction pills uk [url=https://acucarenorthshorewellness.com/pharmacy/Extra-Super-Viagra.html]buy 200 mg extra super viagra amex[/url].

If a regional procedure is to be carried out, the aesthetic unit must be blended inside its boundaries for optimal camouflage. In truth, the mineralization can be poor within the big toe, making it diffcult to analyze 21. Nonmelanoma skin cancer in solid organ transпїЅ plant recipients: replace on epidemiology, threat components, and administration medications side effects prescription drugs [url=https://acucarenorthshorewellness.com/pharmacy/Cyklokapron.html]order online cyklokapron[/url]. Back and extremities Pain and aching in lumbar area; aching of legs; in massive toe. Revamping curricula col- laboratively with other well being professions faculties (Mezey et al. Patients should be given the chance to debate the contents of the Medication Guide and to acquire answers to any questions they may have erectile dysfunction doctors in tallahassee [url=https://acucarenorthshorewellness.com/pharmacy/Levitra-with-Dapoxetine.html]purchase levitra with dapoxetine online pills[/url].

This is equivalent to an estimated average annual price of six injuries per a hundred person-24 years of employment. Objective ninety nine: Utilize data collected in the 2005-07 mountain quail examine to help decide distribution of potential mountain quail habitat in Washington by 2013. The most frequent reasons for admission have been comparable: respiratory syncytial virus, pneumonia, eczema, and fever erectile dysfunction ear [url=https://acucarenorthshorewellness.com/pharmacy/Cialis-Soft.html]cialis soft 40 mg buy[/url]. Insulin (solely regular insulin) is infused at a sluggish, continuous fee (eg, 5 units per hour). The patient was on maintenance dose of lithium which required discontinuation at a later interval secondary to an episode of renal failure. Technical notes Vascular access may be obtained by way of arteriovenous fistulas or grafts used for dialysis impotence under 30 [url=https://acucarenorthshorewellness.com/pharmacy/Levitra-Professional.html]order levitra professional on line amex[/url].

This maneuver is assumed to decrease the house between the head of the humerus and acromion process. The juice of bitter orange has been utilized in For a attainable interplay of supplements containing bitter research of drug metabolism as a comparator to grapefruit orange with caffeine, leading to opposed cardiac effects, see juice, but it is not used as a drugs or beverage. Urine testing is not and tough, and feasible for patients with renal failure (e gestational diabetes test vancouver [url=https://acucarenorthshorewellness.com/pharmacy/Precose.html]purchase precose 50 mg on line[/url]. While it is acknowledged that balancing competing interests is profoundly complex, the extent of the responsibility of look after the complete well being care staff could be judged on a case-by-case basis if the choices have been to be examined by the court docket. When the specimen volume is lower than required have been implicated as etiologic agents of pericarditis and for a number of take a look at requests, prioritization of testing should be myocarditis. Consumer representatives are additionally extensively engaged and are partnering in the guideline translation activities birth control 2 periods in one month [url=https://acucarenorthshorewellness.com/pharmacy/Levlen.html]generic 0.15 mg levlen[/url].

Cloning and developmental expression evaluation of chick Hira (Chira), a candidate gene for DiGeorge syndrome. Rifampin activates hepatotocyte pregnane subsequently metabolized to five-hydroxy-pyrazinoic acid by xan- X receptors, resulting in induction of cytochromes. It is a typical speculation in bioethical debates that the separation between the act of sexual activity and the objective of human procreation will turn into normalised, with the result that, in the distant future, much and even most human copy shall be managed by specialist scientists, so as to safe the potential dad and momпїЅ most well-liked consequence pulse pressure 74 [url=https://acucarenorthshorewellness.com/pharmacy/Lasix.html]lasix 100 mg purchase fast delivery[/url]. Aggressive measures to stop and deal with acute (respiratory) infections (hand washing, immunization, immediate use of antibiotics) should be instituted for an optimal outcome. People often describe it as However, you cannot be sure of the trigger feeling like a curtain has fallen over one until your symptoms are investigated by a eye. Side results: these are usually dose related and could also be troublesome to distinguish from the underlying illness allergy treatment home remedies [url=https://acucarenorthshorewellness.com/pharmacy/Periactin.html]periactin 4 mg order fast delivery[/url].

Journal of Hepatology 1998; Grover 2017 published and unpublished data 28:856�sixty four. There are some variations in protection of orphan medication across different types of Part D plans. I hereby verify that the dissertation “Dynamics of Amyloid Plaque formation in Alzheimer’s disease” is the results of my own work and that I even have solely used sources or supplies listed and specified in the dissertation virus 888 [url=https://acucarenorthshorewellness.com/pharmacy/Suprax.html]purchase discount suprax online[/url]. Happe S, Vennemann M, Evers S, Berger K: Treatment want of is a threat issue for dying in sufferers with stroke. Decision Maximum certification — 2 years Page one hundred forty four of 260 Recommend to certify if: • the underlying systemic metabolic dysfunction has been corrected. Low protein of top quality reduces intestinal ammonia and fragrant amino acid manufacturing treatment regimen [url=https://acucarenorthshorewellness.com/pharmacy/Norpace.html]generic norpace 100mg on line[/url].

Standard radiation remedy utilizes x-rays which deposit nearly all of the radiation dose immediately upon coming into the physique whereas touring to the tumor. Methods of Data Collection a hundred and fifteen (v) Follow-up programme to find out effectiveness of the therapy utilized. In some embodiments, the invention provides methods of treating and/or stopping vascular dementia yawning spasms [url=https://acucarenorthshorewellness.com/pharmacy/Robaxin.html]robaxin 500 mg overnight delivery[/url]. He should obtain a chest x-ray to go alongside Parkland formula for burn resuscitation. Serving dimension/portion dimension per client is defned in diferent ways within the literature. Do not write your Action Plan as one thing to please your provider, household or friends depression iq test [url=https://acucarenorthshorewellness.com/pharmacy/Wellbutrin.html]wellbutrin 300 mg purchase without a prescription[/url].

Markedly diminished effect with continued use of the identical amount of the substance (2) Withdrawal, as manifested by both of the following: a. Drop ankle/brachial thesaurus, as planned earlier than averaging the dorsalis pedis and posterior tibial arte- rial pressures, and society with look alive functioning in tangential arterial illness. Their use, aside expediting the research work, has decreased human drudgery and added to the standard of analysis activity antibiotics you cannot take with methadone [url=https://acucarenorthshorewellness.com/pharmacy/Keflex.html]keflex 750 mg on line[/url]. Refexes such because the knee-jerk would return throughout days one to a few, but then become hyperrefexive over the following few weeks. Specific phobia, situational kind, should be identified versus in the pastпїЅ raphobia if the concern, anxiousness, or avoidance is restricted to one of the agoraphobic conditions. These components include a bigger red cell mass at birth, shorter pink cell half life, immaturity of liver enzyme systems, and poor intestine motility promoting increased enterohepatic circulation symptoms your having a girl [url=https://acucarenorthshorewellness.com/pharmacy/Finax.html]purchase 1 mg finax mastercard[/url].

Table of drugs present in breast milk Drug Comment Abacavir Breastfeeding really helpful during first 6 months if no safe various to breast milk Acetazolamide Amount too small to be harmful Acetylsalicylic acid Short course safe in ordinary dosage; monitor toddler; regular use of high doses might impair platelet function and produce hypoprothrombinaemia in toddler if neonatal vitamin K shops low; possible danger of Reye syndrome Aciclovir Significant amount in milk after systemic administration, however thought of protected to make use of Acitretin Avoid Alcohol Large amounts might have an effect on toddler and scale back milk consumption Allopurinol Present in milk not identified to be dangerous Amantadine Avoid; present in milk; toxicity in toddler reported Appendixes 503 Amiloride Manufacturer advises avoid no data obtainable Aminophylline Present in milk irritability in toddler reported Amiodarone Avoid; present in milk in vital quantities; theoretical threat from release of iodine; see additionally Iodine Amitriptyline Detectable in breast milk; continue breastfeeding; antagonistic effects attainable, monitor toddler for drowsiness Amlodipine Manufacturer advises avoid no information obtainable Amoxicillin Trace amounts in milk; protected in usual dosage; monitor infant Amoxicillin + Trace amounts in milk Clavulanic acid Amphetamines Significant quantity in milk. Countries with enough support companies however unsafe blood merchandise: Patients must be referred to international locations with protected blood products. Randomized, double-blind clinical trial to gauge the efficacy of topical tacalcitol and daylight exposure within the treatment of adult nonsegmental vitiligo homeopathic antibiotics for dogs [url=https://acucarenorthshorewellness.com/pharmacy/Minocycline.html]buy minocycline on line[/url]. In a Phase 1 examine, we are going to decide the minimum efficient dose of abiraterone acetate that normalizes androstenedione levels. The friction ridge skin features of creases, furrows, therefore, the details in the two suffcient prints agree. In very uncommon events, pituitary corticotroph tumors show distant metastasis and/or cerebrospinal fluid dissemination, i medicine 95a pill [url=https://acucarenorthshorewellness.com/pharmacy/Levaquin.html]order levaquin us[/url].

Clinical significance of interleukin?1 genotype in effects of multiple oral components on dental implants surfaces. It is finest not to puncture the capacity and thereby growing the propensity to develop hypoxline for administering medications or changing fuid. Diltiazem therapy with reduced dose of cyclosporine in renal transplant recipients gastritis oatmeal [url=https://acucarenorthshorewellness.com/pharmacy/Prevacid.html]discount prevacid online master card[/url].

Главный принцип профессиональной наркологической помощи — не просто вывести человека из запоя, а стабилизировать организм, предупредить осложнения сердечно-сосудистой системы, печени, почек, головного мозга и нервного баланса. При длительного употребления алкоголя организм теряет жидкость, калий, витамины, нарушается водно-электролитный обмен, повышается нагрузка на сердце, поджелудочную железу и печень. Поэтому лечение запоя должно проводиться индивидуально, с использованием инфузионной терапии, лекарственной поддержки, контроля показателей и рекомендаций для дальнейшего восстановления.

Подробнее тут – [url=https://vyvod-iz-zapoya-v-gelendzhike4.ru/]помощь вывод из запоя[/url]

Здорова, народ Ситуация критическая Дети напуганы Таблетки не помогают Короче, только это реально спасло — выезд нарколога на дом качественно Дал рекомендации и успокоил семью В общем, телефон и цены тут — нарколог на дом круглосуточно [url=https://zapoj.narkolog-na-dom-nizhnij-novgorod-3.ru]https://zapoj.narkolog-na-dom-nizhnij-novgorod-3.ru[/url] Звоните прямо сейчас Перешлите тем кто в такой же ситуации

Эта публикация обращает внимание на важность профилактики зависимостей. Мы обсудим, как осведомленность и образование могут помочь в предотвращении возникновения зависимости. Читатели смогут ознакомиться с полезными советами и ресурсами, которые способствуют здоровому образу жизни.

Познакомиться с результатами исследований – [url=https://likewot.ru/the_articles/alkogol-i-muzhskaya-vneshnost-kak-vypivka-razrushaet-kozhu-figuru-i-privychku-vyglyadet-horosho.html]вывод из запоя куда обратиться[/url]

В данной статье рассматриваются проблемы общественного здоровья и социальные факторы, влияющие на него. Мы акцентируем внимание на значении профилактики и осведомленности в защите здоровья на уровне общества. Читатели смогут узнать о новых инициативах и программах, направленных на улучшение здоровья населения.

Запросить дополнительные данные – [url=https://montisbar.ru/the_articles/kogda-blizkiy-chelovek-v-bede-prakticheskoe-rukovodstvo-po-vyhodu-iz-zapoya-dlya-vsey-semi.html]вывод из запоя с выездом[/url]

Здорова, народ Ситуация критическая Жена в истерике Таблетки не помогают Короче, единственное что вытащило из запоя — вывод из запоя на дому недорого и качественно Поставили капельницу с детоксикационным раствором В общем, жмите чтобы сохранить — капельница от запоя на дому нижний новгород [url=https://alkogolizm.vyvod-iz-zapoya-na-domu-nizhnij-novgorod.ru]капельница от запоя на дому нижний новгород[/url] Вывод из запоя на дому — это реальный выход Перешлите тем кто в такой же ситуации

Hi there, blockchain friends!

Got my hands on a comprehensive piece about AI in trading.

It compares new DeFi apps in blockchain scene.

Really solid perspective.

[url=https://rglinks.org/expert-white-hat-seo-services-with-high-quality-link-building-2707/] See full post [/url]

Llevo como cinco meses con 888starz y la verdad tenia dudas al principio, porque en Espana te cansas de casinos que prometen mucho. Darse de alta me llevo dos minutos, correo, contrasena y listo, y el deposito minimo ronda los unos pocos euros, asi puedes tantear sin jugarte el sueldo.

De tragaperras hay una barbaridad — hablamos de 8.000 juegos de proveedores como Pragmatic Play, NetEnt, Play’n GO, Betsoft y Yggdrasil. Yo tiro mucho de Sweet Bonanza y Book of Dead, eso si tambien le he dado a alguna de Microgaming. La pega es que el filtro por proveedor a veces se atasca cuando el catalogo es tan bestia.

El casino en directo corre a cargo de Evolution y eso se nota: ruletas con crupieres de verdad, Crazy Time y Monopoly Live que enganchan una barbaridad. El bono de bienvenida es de un 130% con 100 tiradas gratis, hay que apostarlo unas 35 veces, que es lo normal del mercado. Tambien hay bonos sin deposito de vez en cuando, puedes mirar lo que hay vigente en [url=https://888starz-es6.com]888starz 1xbet[/url] porque cambian cada mes.

Los cobros va bastante fino. Saque hace poco via e-wallet y lo tuve en 40 minutos. Con tarjeta hay que esperar unos dias, eso ya es cosa del banco. Van con Neteller, Bitcoin y ahi es donde vuela de verdad.

En el telefono cumple, hay APK para Android pero yo uso el navegador y me sobra. La atencion al cliente esta en espanol, no fue instantaneo pero tampoco eterno con una duda de documentacion. La licencia es de Curazao, no esta regulado por la DGOJ espanola y eso cada uno que lo valore. Yo sigo ahi, con sus cosas, aunque las promos hay que leerlas con lupa.